The Vasicek model, named after Oldrich Vasicek, is a mathematical model used in finance to describe the evolution of interest rates over time. It's a type of stochastic differential equation

(SDE) that belongs to the family of continuous-time models used for interest rate modeling.

Key features of the Vasicek model include:

1. Mean Reversion: Like many interest rate models, the Vasicek model assumes that interest rates tend to revert to a long-term mean or equilibrium level over time. This is a common feature used

to capture the behavior of interest rates.

2. Volatility:The model incorporates volatility, allowing interest rates to vary stochastically. This feature accounts for the uncertainty and fluctuations observed in real-world interest rate

data.

3. Speed of Mean Reversion: The Vasicek model includes a parameter that determines the speed at which interest rates revert to the mean. A higher speed of mean reversion implies faster

convergence to the equilibrium rate.

Mathematically, the Vasicek model can be represented by the following stochastic differential equation:

dr(t) = κ(θ - r(t)) dt + σ dW(t)

Where:

- r(t) represents the short-term interest rate at time t.

- κ is the speed of mean reversion.

- θ is the long-term mean or equilibrium interest rate.

- σ is the volatility parameter.

- dW(t) represents a Wiener process, a mathematical construct for modeling randomness.

The Vasicek model has been used in fixed income markets and interest rate derivatives to simulate and analyze interest rate movements. It provides insights into how interest rates evolve over

time and is a fundamental tool in the field of financial mathematics.

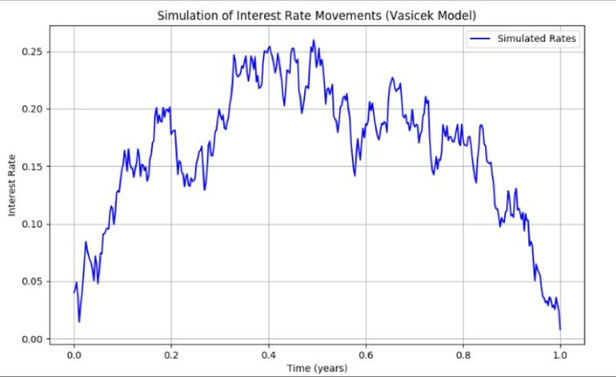

Let's assume the following parameter values for the Vasicek model:

- Long-term mean interest rate (θ): 5%

- Speed of mean reversion (κ): 0.1

- Volatility (σ): 0.2

We'll start with an initial short-term interest rate (r(0)) of 4%, and we want to simulate the interest rate over a short time interval, say, one year, with small time steps (e.g.,

daily).

Using the Vasicek model, you can simulate interest rate changes as follows:

1. Define the time step (Δt) and the number of time steps (N) for the simulation. For this example, let's use Δt = 1/365 (daily) and N = 365 (one year).

2. Initialize an array to store the simulated interest rates. Start with the initial rate: r(0) = 0.04.

3. For each time step (i from 1 to N):

- Calculate a random value from a standard normal distribution (dW(t)) for that time step.

- Update the interest rate using the Vasicek model:

r(t + Δt) = r(t) + κ(θ - r(t))Δt + σdW(t)

4. Repeat step 3 for each time step.

Write a comment