Subadditivity is a principle in risk management that suggests combining two or more risky assets should not result in a total risk greater than the sum of the individual risks. The concept comes

from the idea that diversification typically reduces risk.

The

formula for subadditivity, can be written as:

rho(A

+ B) ≤ rho(A) + rho(B)

Where

"rho" represents the risk measure, and A and B represent different assets or portfolios. If the total risk (rho) of the combined portfolio (A + B) is less than or equal to the sum of the risks of

the individual portfolios (A and B), then the risk measure is considered subadditive.

Subadditivity

is one of the key properties that a risk measure must have to be considered a coherent risk measure.

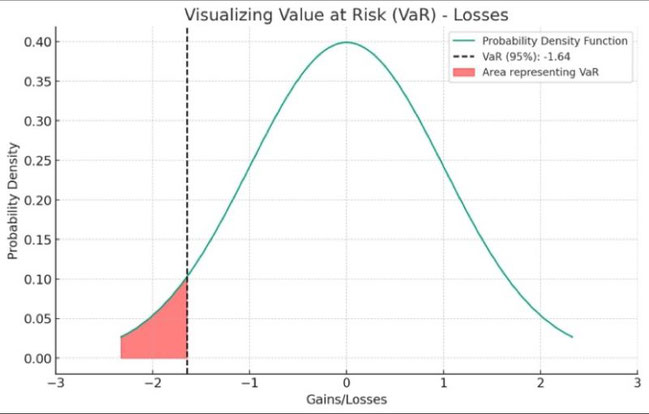

Value

at Risk (VaR) is often criticized for not always satisfying the subadditivity condition.

VaR

is calculated as a specific percentile of the loss distribution — for example, the 95th percentile. This means it only measures the loss that is not exceeded with a certain confidence level (say,

95% of the time).

However,

it doesn't provide any information about the potential size or frequency of losses that exceed this level. In other words, VaR tells us nothing about how "bad" the bad outcomes can be beyond this

point, which is often referred to as the "tail risk."

The

following example illustrates the lack of subadditivity in VaR:

Imagine

2 bonds whose default probability is 4% with a notional value of 10 millions dollars and a loss given default of 100% for each bond.

At

a 95% confidence level, the VaR for each bond individually would be $0 because the default probability (4%) is below our 5% VaR threshold. This means we are 95% confident that the loss will not

exceed $0 due to default.

To

find the probability that neither bond defaults, we multiply the probability that each bond does not default.

For

each bond, this is (1- 0.04), or 96%. So for both: (1- 0.04)* (1- 0.04) = 0.9216

To

find the probability that at least one bond defaults, we subtract the probability that neither defaults from 1:

1

- 0.9216 = 0.0784 or 7.84%.

Since

the probability that at least one bond defaults (7.84%) is greater than our 5% threshold, we must consider the full notional value at risk. Thus, the VaR for the combined portfolio is the full

notional amount, which is $1 0 million.

CVaR

addresses the shortcomings of VaR by providing an average expected loss in the worst-case scenarios beyond the VaR threshold. It takes into account the “shape” and severity of the tail risk,

which VaR ignores. CVaR is sub-additive, meaning it properly reflects the benefit of diversification.

SubadditivityPrinciple

RiskManagementBasics

DiversificationBenefits

FinancialRisk

ValueAtRisk

RiskMeasure

PortfolioRisk

VaRCritique

TailRiskAwareness

ConditionalVaR

Write a comment