Key Takeaways:

- A Wiener process is like a random walk; Sam and Tina’s steps are random, similar to coin flips.

- Cov(W_s, W_t) = min{s, t} represents their joint movement over time.

- Their covariance only covers the shared time walking; any extra steps beyond that don’t count.

- The shared duration of their walk, not individual steps, determines their joint variability.

- The variance of their paths is tied to the time they walk together, emphasizing their intertwined journey.

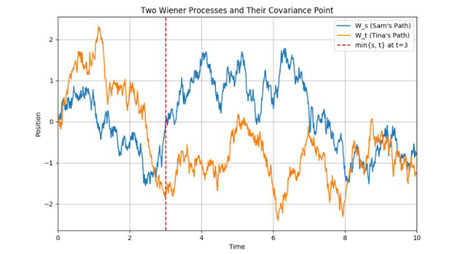

Picture two friends, Sam and Tina, taking such a walk.

Both Sam and Tina start at the same location in the park and begin their walk simultaneously. Their next step is entirely random, much like flipping a coin: a head might mean taking a step forward while a tail could signify stepping back.

Mathematical FormulationThe Wiener process, also known as Brownian motion, is a continuous-time stochastic process \( W_t \) that satisfies the following properties:

- \( W_0 = 0 \).

- \( W_t \) has independent increments: for any \( 0 \leq s < t \), the increment \( W_t - W_s \) is independent of the past \( W_u \) for \( u \leq s \).

- \( W_t \) has Gaussian increments: \( W_t - W_s \sim \mathcal{N}(0, t - s) \).

- \( W_t \) has continuous paths almost surely.

The covariance structure of the Wiener process is given by:

\[ \text{Cov}(W_s, W_t) = \min(s, t) \]

which indicates that the covariance of two time points is determined by the minimum of those times.

Interpretation of CovarianceCovariance measures the joint variability of two processes. Here, it reflects how two Wiener processes, starting together, evolve over time.

Consider two time points, \( s \) and \( t \):

\( W_s \) reflects where Sam is at time \( s \), and \( W_t \) represents Tina's position at time \( t \).

Step-by-Step Explanation1. If Sam's random walk lasts 5 minutes (\( s=5 \)) but Tina stops at 3 minutes (\( t=3 \)), the time they walked together is only 3 minutes.

Mathematically, the covariance is:

\[ \text{Cov}(W_5, W_3) = \min(5,3) = 3. \]

2. If Tina had walked up to 6 minutes, then:

\[ \text{Cov}(W_5, W_6) = \min(5,6) = 5. \]

This means that the common randomness in their walks is dictated by the time spent together, not the individual step randomness.

Variance and IndependenceSince \( W_t \) is a standard Wiener process, its variance follows:

\[ \text{Var}(W_t) = t. \]

Furthermore, the increments are independent:

\[ W_t - W_s \sim \mathcal{N}(0, t-s), \quad \text{for } 0 \leq s < t. \]

This property ensures that steps taken after a given time \( s \) do not influence the previous values.

ConclusionThe covariance formula \( \text{Cov}(W_s, W_t) = \min(s,t) \) encapsulates how two Wiener processes share randomness only during their overlapping time.

The relationship is about the shared duration and joint variability within that timeframe, rather than the specifics of individual movements.

Écrire commentaire